Being in the wrong super fund can cost you hundreds of thousands of dollars, so it pays to check that your fund is performing. Up until recently, this was more easily said than done. But last year, the government introduced a series of reforms that equip consumers with the resources to make better choices.

One of these reforms is an annual performance test that reviews super funds’ long term performance to make sure they’re helping build people’s retirement balances. The test currently only covers the default super products (called MySuper). The Government wants to review the test before expanding it to include ‘choice’ (called Trustee Directed Products).

Products that failed the performance test in 2022:

Products that failed the first test, in 2021:

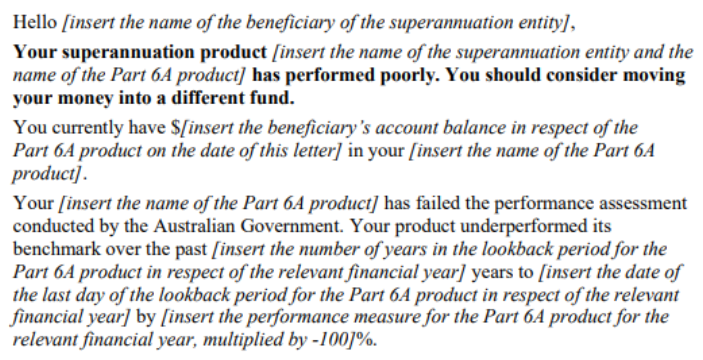

Funds were required to tell their members they had failed

In the second half of 2021, the government named 13 funds whose default MySuper products failed the annual performance test. As a direct consequence of a first failure, the new law required funds to let their members know they had failed this test and that they should consider moving to a new product. If a product fails a second time consecutively, it must be closed off to new members.

In 2022, five funds failed and each must write to its members advising them of the product’s failure. Funds’ letters must include legislative prescribed text. The wording could be even more direct to incite action, but it is largely suitable in explaining the funds performance. It includes a rule of thumb on performance and directs people to the comparison tool. An extract is below:1

The regulator warned funds – Don’t be misleading and/or deceptive

ASIC wrote to funds that failed the test, warning that it would be undertaking reviews to ensure compliance with the intent of the reforms and the legislative requirements for communications. ASIC was clear in its messaging about the letter and websites.

With the reforms being about providing transparency and protecting people from underperforming products, funds were put on notice not to undermine the intent of these communications.

ASIC released the findings of its review in June this year. It found the communication strategies of some trustees strictly complied with the disclosure obligations, however, they also “may have risked confusing or misleading members about their product’s performance.”3 We agree with the regulator and this evidence raises questions about the adequacy of the disclosure obligations in protecting consumers from poor performance.

ASIC’s REP 729 identifies communication strategies of concern including, for example:

publishing the MySuper product’s failure of the test on a webpage less likely to be visited by persons interested in the product;

highlighting other performance measures that were more favourable, such as recent positive past performance figures; or

criticising aspects of the test to suggest it was not relevant to the particular product.

Super Consumers Australia – Fact Check

Super Consumers Australia decided to take a closer look at two examples in the market – a letter provided by Fund A, and the website of Fund B – and analyse how a consumer might perceive them. Here is our fact check on some of the more confusing claims they made to members.

Fund A – Letter to members

Fund A’s government-mandated template appeared after four pages of fund-created content. This was the fund’s attempt to provide members with additional information to help them understand the performance test. But much of the content went to the benefits of being a member of the fund and the fund’s outperformance of its objectives. This language conflicts with the intent of the letter which aims to move members out of underperforming products. Some of the worst examples are below:

The claim – Our returns exceed our targets

“We often say that past performance is no guarantee of future performance, which is important to consider as the performance test applies to investment performance over the past seven years. … (Our product) has delivered returns in excess of the investment objectives that were established when the fund was set up in 2013, which has aimed to deliver a return of between 1.0% and 3.0% above inflation (CPI), depending on your age.

Implication

That the product and the member’s stage is outperforming on at least one relevant metric. This suggests to the reader that the investment performance of the fund is better than the test has measured.

Commentary

In the same paragraph in which Fund A states that past performance isn’t a reliable indicator, they go on to note that their past performance has been exceeding self-set targets. This is used as persuasive evidence of performance.

Target returns are also a weak test of a product’s investment performance. The Productivity Commission found that all the MySuper products it tested outperformed their median target return over four years.4 Fund A’s 1970’s lifestage also had the joint lowest target return of a peer group of ‘1970’ life-stage products, while also disclosing the highest level of investment risk.5 This finding suggests that the self-set target return is an especially weak test for Fund A.

The claim – Our one year product level returns rank favourably against a ratings agency sample

“(Our product) has delivered an average return of 22.4 per cent for members over the 12 months to 30 June 2021. In the Rainmaker Selecting Super rankings of Workplace Super (Our product) was ranked third for performance for the year to 30 June 2021. … One of the country’s best performing products over the 12 months.

Implication

That the product is outperforming most peers over the short-term. The reader is left with the impression that over the short-term, their fund performs well, or is ‘turning around’ its past underperformance.

Commentary

Fund A has given prominence in their letter to a particular time period over which they appear to perform well. The fund doesn’t provide the important context that super fund returns in the financial year 2020-21 were well above its long term average6, following external factors, such as the rebound in equity markets after their 2020 slump in the wake of COVID.

For most members, superannuation is a long-term investment. Focusing on one-year returns seems designed to put the product in the best possible light and runs against the norms of super fund comparisons.

The Claim – We have been awarded a wide range of trophies, awards and rankings

“You have access to our FirstBenefits program”

Implication

That the fund is externally recognised as a high performer, suggesting that the fund may have failed the test this year, but are a top performer on other (non-performance based) metrics.

Commentary

The use of trophy images, awards and rankings is highly inappropriate in a letter that is supposed to communicate that a product has failed a performance test. It undermines the intent of the letter and crosses into advertising material.

The material also attempts to maintain members with its rewards program, which includes theme park tickets. This is completely unrelated to fund performance and retirement benefits.

The claim – We have performed well against our peers

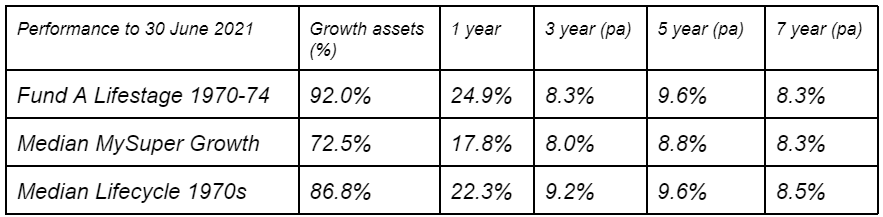

“Members in (your stage of our lifecycle product) enjoyed returns of 24.54% after fees and taxes for the 12 months to 30 June 2021. (Our product) has performed well against MySuper peer funds. … Returns are competitive with other MySuper funds … Comparison to the Chant West survey of MySuper funds (note that the survey does not include administration fees)

Implication The product and lifestage the reader is in performs well against its peers and had a large return over the last financial year. The reader is likely to think they are in a better product than the alternatives.

Commentary The statement that the product has performed well against MySuper peer funds potentially undermines the purpose of the performance test. The table with performance data refers to the lifestage the member is in and not the product and cannot be used to substantiate that claim.

With regards to the table, the comparison of the lifestage with the median MySuper growth option is inappropriate. The growth asset allocation of the product is 19.5 percentage points higher than the allocation of the median growth option. As a result the lifestage product is likely taking on substantially more risk than the benchmark to which it is being compared. This isn’t comparing ‘apples with apples’.

Comparing the lifestage with the median 1970s lifestage is a more reasonable comparison as these stages are all aimed at the same audience. However, the Fund A stage has underperformed its peers over three, five and seven years.

The data also excludes admin fees. Not using net return figures in peer comparisons is inappropriate as it does not give an accurate picture of relative performance.

Fund B – Website communications

Funds must make publicly available on their website that their MySuper product failed the performance test.

The following is an analysis of some of the FAQs on Fund B’s web page on the Your Future Your Super performance test on the 2nd of September 2021. Please note the FAQ has subsequently been updated.

FAQ: Is Fund B a poorly performing Superannuation Fund?

“(Fund B) has underperformed relative to the legislated benchmark in the YFYS test for the Fund’s strategic asset allocation over the 7 year period. The graph below outlines where Fund B’s Growth (MySuper) option sits against other funds’ MySuper products, investment returns for the same period after fees and tax.

Implication

The graph shows Fund B only slightly below a performance trend line. The reader may be left thinking the fund has only slightly underperformed relative to its peers.

Commentary

The graph shows the fund’s risk-adjusted performance relative to its peers, not its performance against the test. A reader may confuse the two and conclude the fund’s underperformance is mild. In fact, the fund underperformed the benchmark portfolio by 78 basis points, failing the test by 28 basis points.

The text does not explicitly answer the question posed and it is left to the reader to conclude.

FAQ: Why did you underperform when the current year is so good?

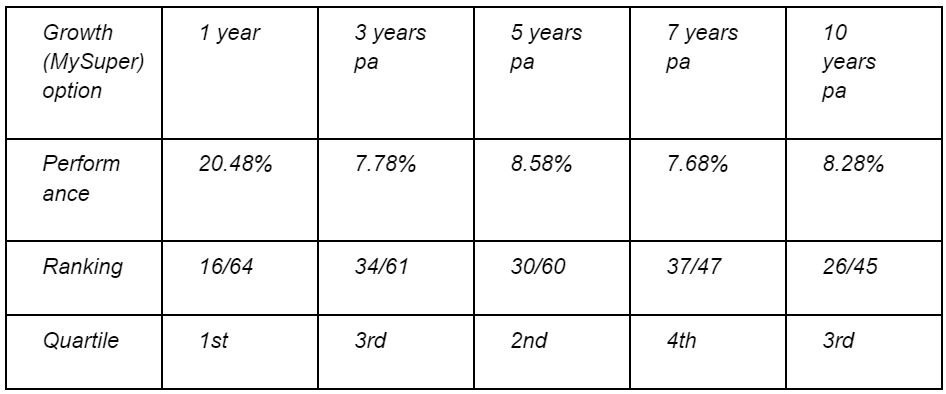

“There are different ways of looking at performance returns. You can look at performance over different time frames, say 2, 5 or 10 years.

The data below is provided by Rainmaker and compares Fund B’s MySuper option to most other MySuper products. (Large employer funds and a few others are excluded).

As you can see, depending on the timeframe, you get a very different result.

Implication The MySuper option is a good performer over some periods, and a poor performer over others, so the timeframe of comparison is important. In the context of the rest of the FAQ, the reader may begin to question why the test is over seven years if performance varies so much by time period considered. This is despite the fact that the table measures against peer performance, not the performance test. In the context of underperformance against the test, comparison to the returns of MySuper ‘peers’ may give an inaccurate picture of the value the trustee has added. This comparison may simply reflect a different underlying asset allocation. The information also omits the important context that long-term performance is a better guide for consumers with long-term investment goals, which is likely to be the goal of most members in this product.

Commentary This section lacks a lot of important context. For most, super is a long term investment, and readers should not put weight in short-term returns. In Fund B’s case, the overall performance of the fund against its peers is below average (4th and 3rd quartile for 7 and 10 year returns).

The use of “underperformance” in the FAQ also repeatedly conflates two separate measures of underperformance. In some cases, it compares the product to other MySuper products while at other times, it refers to underperformance against the test, which is based on a passive reference portfolio.

FAQ: Are Fund B’s fees high compared to other industry funds? “The fees you pay are dependent on the products you are invested in and your account size.

We are always looking for opportunities to reduce fees and have reduced both admin and investment fees in the last 18 months.

In fact, we will be announcing a fee cap for high balance accounts in the coming weeks.

Implication That fees are being reduced, and caps will be in place to prohibit high fees.

Commentary Despite the reductions the fees paid still remain above average for the product type. As of June 2021 (latest data when page was last updated), Fund B had a fee of 1.21% on a $50,000 balance, compared to a median fee of 1.07%.7 This result puts it in the top quarter of all funds in terms of its total fee.

Fund websites 6 months on

Super Consumers Australia also undertook a project to assess underperforming funds’ webpages six months on from the performance test. We sought to understand what fund communications a member may read if they: searched for information on their fund’s performance; or visited their fund’s homepage.

Three of the 13 funds that failed the first round had either merged or closed and no longer had a web presence at the time of this review. We expected the remaining 10 to still be honestly addressing their recent underperformance and the actions they have taken to improve.

First organic search result: 60% don’t mention failure Search Engine Optimisation (SEO) analysis from CHOICE’s SEO expert revealed that the main search people use to find out about a specific super fund’s performance is ‘fund name + performance’. Using this search term in private browsing mode (to lower the possibility of tailored results), we analysed the first organic (unpaid) result of each search.

Of the remaining 10 funds, six did not mention their failure in the performance test on the first page that appeared in the search results. This omission makes it hard for consumers to find information on the fund’s performance test failure. A typical consumer is unlikely to search far beyond the fund website they are directed to on performance, so would be unlikely to realise the product had failed the test. Fund homepages: 40% did not mention failure

Four funds did not mention their failure on their homepage. The remaining six communicated their failure on their homepage with text that mentioned underperformance and a link to more information. One fund linked to information on their underperformance in neutral language. For example, their homepage has a link to the neutrally-titled ‘FY21 super performance’. This takes the reader to a blog post headlined by the fund’s “strong one-year returns for MySuper members”. A reader could be forgiven for thinking that, far from failing its performance test, the fund is performing at an historically strong level. The post also focuses exclusively on short-term performance, which for most people is less relevant in a long-term investment like super.

Poor communication undermines the test Super Consumers’ analysis has found that the flexibility granted to trustees regarding the content of the letter has allowed some trustees to obfuscate the true purpose and clarity of the notification, potentially leading to lower levels of switching. This is in spite of ASIC’s warning to failing funds that “any communication [the fund] makes in relation to the [annual performance assessment] or about [their] performance should provide information in a balanced and factual way that is not misleading and/or deceptive”.

For members or prospective members interested and actively searching their fund to find out how the fund’s MySuper product performs, the performance test result is highly relevant information. Omitting this information is extremely questionable.

The performance test represents a dramatic positive change on the part of super funds to better serve members. The performance test’s objective ‘bright line’ and clear consequences for failure have resulted in substantial fee reductions and driven a new level of consumer-focussed mergers. It should not be undermined by super funds with poor communications, especially as the test is expanded to underperforming choice super products.

The YF,YS review can ensure poor communication is curtailed The Federal Government is reviewing the Your Future, Your Super measures. In this review, the Government asks if the notification and website publication of results have been effective and if they could be improved. Our analysis highlights that super funds will resort to self-preservation when given the opportunity. Thousands of members may have been misguided through the provision of fund-created content.

Failing funds should not be permitted to add additional content to the underperformance letter; additionally, they should be required to display a prominent notice on their website homepage until the product/s have passed the performance, or are no longer in the market. While the SIS Act and Regs require failing funds to host, and keep up to date, a description of circumstances surrounding their performance test failure, it is clear a more prescriptive approach is needed to ensure poor communication is curtailed.

In our submission to Treasury, we also suggest some tested improvements to the standard information in the underperformance notification to ensure that it encourages action.8 It is important for the standard information to undergo targeted consumer testing to ensure it is appropriate for a diverse range of audiences. To increase the reach of the underperformance notification, we also suggest that customers of underperforming funds are notified with the standard information via a message in their MyGov inbox. This is in line with findings about consumers’ communication preferences in the ATO’s recent YourSuper tool research.9

Recommendations: That failing funds are explicitly prevented from issuing performance test failure notifications that include anything other than the standard information. That failing funds are required to maintain a prescribed notification about their underperformance until their product/s have passed the performance test, or are no longer offered. That tested improvements are made to the standard information included in the underperformance notification, including the way in which it is delivered.